Key Takeaways

- Insurance companies generally only pay up to the applicable policy limits, regardless of how severe your injuries may be.

- If your medical bills and other damages exceed available coverage, additional compensation may be available through other insurance policies or liable parties.

- Health insurance, Medicare, Medi-Cal, and medical liens can help cover treatment costs while your personal injury claim is pending.

- Potential sources of additional recovery include underinsured motorist (UIM) coverage, umbrella policies, employer liability, and claims against other legally responsible parties.

- Before you accept a settlement, determine all available insurance coverage and fully assess your current and future damages.

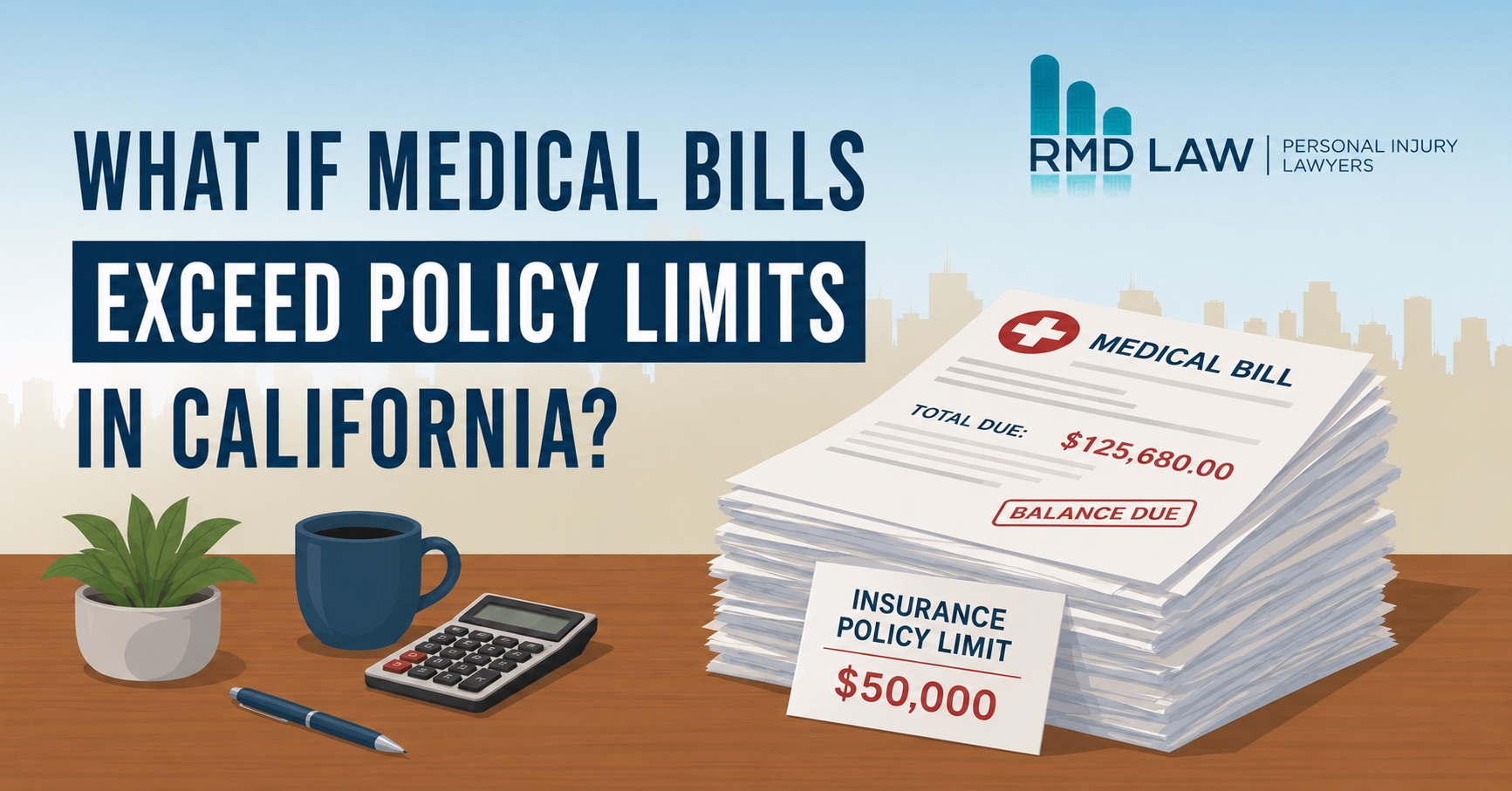

What Happens If My Medical Bills Exceed the Insurance Policy Limits?

Many accident victims assume the at-fault driver’s insurance company will pay for all of their medical bills and other losses. In reality, insurance policies contain contractual limits that cap the amount an insurance company is required to pay, regardless of how serious an accident is. California recently increased its minimum auto insurance requirements from $15,000 to $30,000 under Senate Bill 1107. However, these minimums still fall far below the cost of many serious injury cases.

This situation is especially common in catastrophic injury cases involving emergency surgery, extended hospital stays, traumatic brain injuries, spinal cord injuries, permanent disabilities, or long-term rehabilitation. Reaching an insurance policy limit does not necessarily reflect the full extent of available insurance coverage in a serious injury case.

Understanding how insurance limits interact with injury claims is key to identifying potential recovery options under California law.

Who Pays My Medical Bills If Insurance Isn’t Enough?

One of the biggest concerns after a serious accident is how ongoing medical treatment will be paid while a personal injury claim is still pending. Medical providers typically continue billing for treatment during this time, which means injured patients often need a temporary source of payment while their case is ongoing.

Health Insurance

If you have private health insurance, it is often the primary source of payment for accident-related treatment while a claim is pending.

Although deductibles and copays may still apply, using your health insurance can help ensure you continue receiving necessary treatment without waiting for a settlement.

Your health insurer typically has the right to seek reimbursement from any settlement you recover, depending on the terms of your policy.

Medicare and Medi-Cal

If you qualify for Medicare or Medi-Cal, these programs often also pay for accident-related treatment.

Like private health insurance, these programs may have reimbursement rights if you later recover compensation from the at-fault party. Properly resolving these reimbursement obligations is often an important part of settling a personal injury claim.

Medical Liens

Some doctors, specialists, and treatment facilities agree to provide medical care on a lien basis.

Rather than requiring payment upfront, they agree to wait until your case resolves before collecting payment from your settlement. Medical liens are commonly used in California personal injury cases when injured victims need treatment but cannot afford to pay out of pocket.

In many injury cases, part of the resolution process involves negotiating reductions of medical liens and reimbursement claims, which can significantly increase how much of a settlement ultimately goes to the injured person.

Am I Responsible for Medical Bills That Exceed My Settlement?

Potentially, yes.

If your settlement does not fully cover your medical expenses, you could be responsible for unpaid balances. Responsibility often depends on how treatment was billed (insurance, lien, or self-pay) and whether reductions or reimbursements are negotiated as part of the settlement process.

How Can I Recover Compensation Beyond the Insurance Policy Limits?

Additional insurance policies or other legally responsible parties may provide opportunities to recover compensation beyond the at-fault driver’s primary insurance policy.

Underinsured Motorist Coverage (UIM)

If you purchased underinsured motorist (UIM) coverage as part of your own auto insurance policy, it may help cover damages when the at-fault driver’s insurance is not enough.

For example, if the other driver carries California’s minimum bodily injury liability coverage of $30,000 per person and you carry higher UIM limits, your own policy can provide additional compensation once the at-fault driver’s coverage is exhausted, subject to policy terms.

Umbrella Insurance Policies

Some individuals carry umbrella liability insurance that provides coverage beyond the limits of a standard auto or homeowners policy.

For example, a driver might have $100,000 in auto liability coverage and a $1 million umbrella policy, significantly increasing available insurance coverage in qualifying cases.

Employer Liability Coverage

If the driver who caused the accident was working at the time of the collision, additional commercial insurance coverage may be available.

Examples include accidents involving:

- Delivery drivers

- Commercial trucks

- Utility or service vehicles

- Construction company vehicles

- Employees driving for work-related purposes

Multiple Liable Parties

Some accidents involve more than one negligent party.

When multiple parties share responsibility, possibilities for additional insurance policies become available, increasing the total compensation that can potentially be recovered.

For example, in a multi-vehicle crash involving two negligent drivers, each may carry separate insurance policies. If Driver A carries $100,000 in coverage and Driver B carries $100,000 in coverage, both policies could be available depending on how fault is allocated. This can significantly increase total compensation compared to a single-policy claim.

Can the At-Fault Party Be Personally Liable?

If insurance coverage is insufficient, there is a possibility to pursue the at-fault party personally for the remaining damages.

Whether doing so is worthwhile depends largely on whether the individual has collectible assets beyond available insurance coverage. While a court judgment may establish legal liability, collecting on that judgment is not always practical if the defendant lacks significant assets.

What If Future Medical Treatment Costs More Than the Available Insurance?

Medical bills do not always end when a case settles.

Many serious injuries require long-term or ongoing care, including future surgeries, rehabilitation, pain management, assistive devices, or other forms of continued treatment.

In addition to future medical expenses, an injured person could also face:

- Reduced earning capacity

- Permanent disability

- Ongoing rehabilitation costs

- Lifetime care needs

In catastrophic injury cases, attorneys often work with medical and financial experts to estimate the long-term cost of care. Under California law, injured victims may recover compensation for reasonably anticipated future medical expenses when those losses are supported by competent medical evidence.

What Should You Consider Before Accepting an Insurance Settlement?

One of the most common mistakes we see accident victims make is assuming the first available insurance policy represents the full amount they can recover.

Before resolving a serious injury claim, it is important to evaluate:

- Every applicable insurance policy

- All available insurance coverage, including potential third-party or supplemental policies

- The full extent of current and future damages

A complete claim valuation must account for more than current medical bills. It should also include future medical treatment, lost wages, diminished earning capacity, pain and suffering, and other long-term consequences of the injury.

Settling too early can result in compensation that does not fully account for expenses that arise later.

Conclusion

When medical bills exceed available insurance coverage, it does not necessarily mean your options are limited. Many serious injury cases involve additional sources of compensation that are not immediately obvious at the outset.

The key is understanding the full extent of your injuries and identifying all potentially responsible parties and available insurance coverage before any settlement is finalized.

If you are dealing with serious injuries and are unsure whether all potential sources of compensation have been explored, it is often worth having your case reviewed before making any decisions.

Our team at RMD Law offers free consultations and can help you understand your options moving forward.

FAQs

Not necessarily. An initial settlement offer does not always fully account for future medical expenses, lost income, or other damages. Before accepting any offer, it’s important to understand the full value of your personal injury claim, as settlements are generally final.

Insurance companies are not required to automatically offer their policy limits. They may dispute fault, question your injuries, or challenge the value of your claim. If a fair settlement cannot be reached, additional legal action could be considered.

Often, yes. Hospitals, medical providers, and lienholders agree to reduce outstanding medical bills or reimbursement claims after a settlement, helping you keep more of your compensation.

Yes. You do not need to know the at-fault driver’s insurance policy limits before filing a personal injury claim. The available insurance coverage is typically identified during the claims process, and starting your claim promptly can help preserve evidence and protect your legal rights.

In most cases, California law gives injured victims two years from the date of the accident to file a personal injury lawsuit. However, shorter deadlines may apply in certain cases, including claims against government entities.